This tutorial will explore how to perform regularized multinomial logistic regression in R. We will cover both the manual approach—building the model from scratch—and using the popular {glmnet} package. The {glmnet} package is widely used for fitting generalized linear models with elastic net regularization and offers efficient algorithms for solving penalized regression problems. By the end of this tutorial, you will thoroughly understand how to fit regularized multinomial logistic regression models in R, both by manually implementing the model and utilizing the efficient {glmnet} package for regularized model fitting. Mastering regularized multinomial logistic regression is an essential skill for any data scientist or statistician, whether you are working with high-dimensional data or aiming to improve the interpretability of your models.

Overview

Multinomial Logistic Regression (MLR) is an extension of binary logistic regression used when the dependent variable \(y\) is categorical with more than two levels (e.g., \(C\) classes, \(y \in \{1, 2, \dots, C\}\)). Regularization is added to the optimization process to prevent overfitting by penalizing large coefficients. To prevent overfitting, regularization is introduced by adding a penalty term to the likelihood function.

The common regularization techniques are:

Ridge Regularization (L2)

Adds a penalty proportional to the square of the coefficients:

Use metrics like accuracy, cross-entropy loss, or confusion matrix to evaluate performance.

Regularized Multinomial Logistic Regression from Scratch

Fitting a regularized multinomial logistic regression in R without using external packages can be achieved by manually implementing the necessary steps, as R does not natively provide multinomial logistic regression with regularization in base functions. Here’s a comprehensive guide to perform this task:

Synthetic Data Generation

We will generate a synthetic dataset with three classes and multiple predictors.

Code

# Set seed for reproducibilityset.seed(42)# 1. Generate synthetic datan <-300# Number of observationsp <-10# Number of predictorsk <-3# Number of classes# Generate predictorsX <-matrix(rnorm(n * p), n, p)# Generate coefficientsbeta <-matrix(rnorm(p * (k -1)), p, k -1)# Compute linear predictors and probabilitieseta <-cbind(0, X %*% beta) # Linear predictors for k-1 classesprob <-exp(eta) /rowSums(exp(eta)) # Convert to probabilitiesy <-apply(prob, 1, function(x) sample(1:k, 1, prob = x)) # Multinomial responsedata <-data.frame(y =as.factor(y), X)head(data)

Create a 5-fold cross-validation setup and define the hyperparameters for regularization.

Code

# 2. Cross-validation setupfolds <-sample(1:5, n, replace =TRUE) # 5-fold cross-validationalphas <-seq(0, 1, by =0.1) # Elastic net mixinglambdas <-10^seq(-4, 1, length =10) # Regularization strengths

Create Loss Functions and Optimization

Define the loss functions for Ridge, Lasso, and Elastic Net regularization. The loss functions compute the negative log-likelihood of the multinomial logistic regression model with the penalty term.

Code

# 3. Loss functions for regularized multinomial logistic regressionridge_loss <-function(beta_vec, X, y, lambda, k) { n <-nrow(X) p <-ncol(X) beta <-matrix(beta_vec, p, k -1)# Compute linear predictors and probabilities eta <-cbind(0, X %*% beta) prob <-exp(eta) /rowSums(exp(eta))# Multinomial negative log-likelihood log_lik <--sum(log(prob[cbind(1:n, as.numeric(y))]))# Ridge penalty ridge_penalty <- lambda *sum(beta^2)return(log_lik + ridge_penalty)}lasso_loss <-function(beta_vec, X, y, lambda, k) { n <-nrow(X) p <-ncol(X) beta <-matrix(beta_vec, p, k -1)# Compute linear predictors and probabilities eta <-cbind(0, X %*% beta) prob <-exp(eta) /rowSums(exp(eta))# Multinomial negative log-likelihood log_lik <--sum(log(prob[cbind(1:n, as.numeric(y))]))# Lasso penalty lasso_penalty <- lambda *sum(abs(beta))return(log_lik + lasso_penalty)}elastic_net_loss <-function(beta_vec, X, y, lambda, alpha, k) { n <-nrow(X) p <-ncol(X) beta <-matrix(beta_vec, p, k -1)# Compute linear predictors and probabilities eta <-cbind(0, X %*% beta) prob <-exp(eta) /rowSums(exp(eta))# Multinomial negative log-likelihood log_lik <--sum(log(prob[cbind(1:n, as.numeric(y))]))# Elastic net penalty ridge_penalty <- (1- alpha) * lambda *sum(beta^2) lasso_penalty <- alpha * lambda *sum(abs(beta))return(log_lik + ridge_penalty + lasso_penalty)}# Gradient descent optimization for Ridge, Lasso, and Elastic Netoptimize_model <-function(X, y, lambda, alpha =NULL, k, loss_function) { p <-ncol(X) beta_init <-rnorm(p * (k -1))# Pass alpha only for Elastic Netif (is.null(alpha)) { optim_res <-optim(beta_init, loss_function, X = X, y = y, lambda = lambda, k = k, method ="BFGS") } else { optim_res <-optim(beta_init, loss_function, X = X, y = y, lambda = lambda, alpha = alpha, k = k, method ="BFGS") }return(matrix(optim_res$par, p, k -1))}

Hyperparameter Selection via Cross-Validation

Perform hyperparameter selection via cross-validation to find the best model and hyperparameters.

In R, you can perform multinomial logistic regression using the {glmnet} package, which fits a generalized linear model via penalized maximum likelihood. {glmnet} supports ridge regression, lasso regression, and elastic net for various types of generalized linear models, including multinomial logistic regression.

The response variable y must be a factor for multinomial regression.

The family = "multinomial" argument ensures that the model performs multinomial logistic regression.

glmnet handles both Lasso (alpha = 1) and Ridge (alpha = 0) penalties, or you can use an Elastic Net combination by setting 0 < alpha < 1.

In this tutorial, we will demonstrate how to perform regularized multinomial logistic regression in R using the {glmnet} package. We will use the health_insurance data set, which contains information about individuals’ choice of health insurance products based on their

Install Required R Packages

To fit a Regularized Logistic Model R, we will use {glmnet} package. The {glmnet} package provides efficient functions for fitting generalized linear models (GLMs) with L1 (Lasso) and L2 (Ridge) regularization. The package is widely used for regression and classification tasks, especially when dealing with high-dimensional data or multicollinearity.

Following R packages are required to run this notebook. If any of these packages are not installed, you can install them using the code below:

Rows: 1448 Columns: 6

── Column specification ────────────────────────────────────────────────────────

Delimiter: ","

chr (2): product, gender

dbl (4): age, household, position_level, absent

ℹ Use `spec()` to retrieve the full column specification for this data.

ℹ Specify the column types or set `show_col_types = FALSE` to quiet this message.

x for holding the predictor variables. This should be created using the function model.matrix() allowing to automatically transform any qualitative variables (if any) into dummy variables, which is important because glmnet() can only take numerical, quantitative inputs. After creating the model matrix, we remove the intercept component at index = 1.

Now we can apply cv.glmnet() function for cross-validation to choose the best lambda (regularization parameter). For example, suppose we designate \(α\)=0 for ridge regression and specify nlambda as 200. This implies that the model fit will be calculated solely for 200 \(λ\) values.

A special option for multinomial regression is type.multinomial, which allows the usage of a grouped lasso penalty (q=2 ) if type.multinomial = "grouped". The default is type.multinomial = "ungrouped" (q=1 ).

Printing the resulting object gives some basic information on the cross-validation performed:

Code

print(ridge.cv)

Call: cv.glmnet(x = x.train, y = y.train, type.measure = "deviance", nfolds = 5, alpha = 0, family = "multinomial", type.multinomial = "grouped", nlambda = 200)

Measure: Multinomial Deviance

Lambda Index Measure SE Nonzero

min 0.03771 200 1.139 0.01966 6

1se 0.04537 196 1.158 0.01826 6

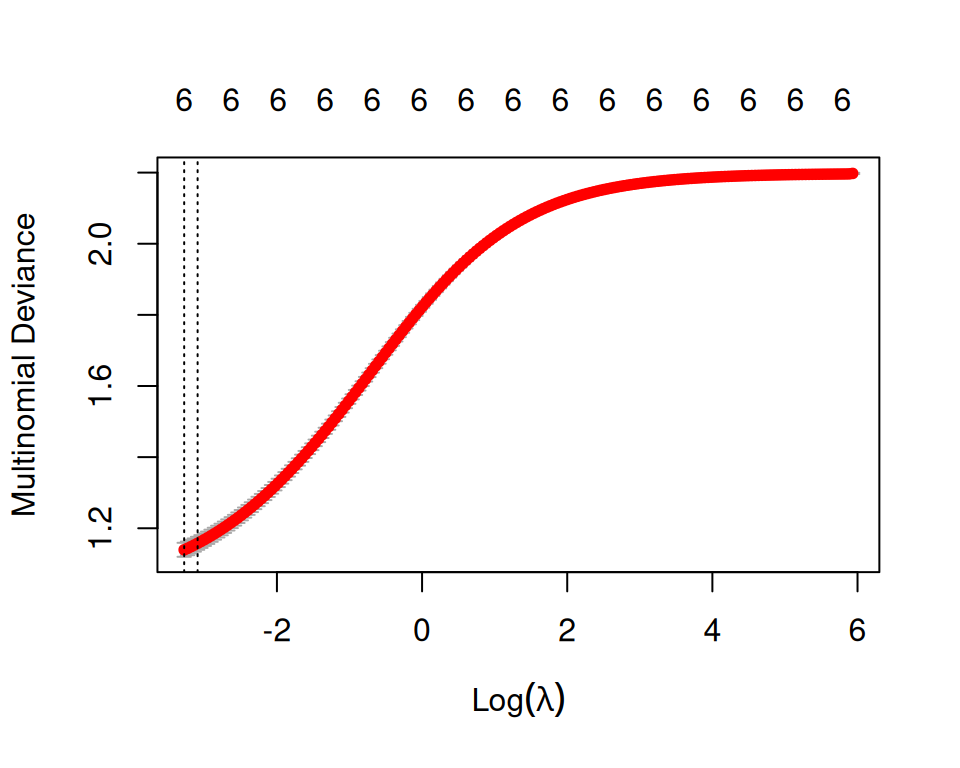

We can plot ridge.cv object to see how each tested lambda value performed:

Code

plot(ridge.cv)

The plot shows the cross-validation error based on the logarithm of lambda. The dashed vertical line on the left indicates that the optimal logarithm of lambda is around -2, which minimizes the prediction error. This lambda value will provide the most accurate model. The exact value of lambda can be viewed as follow:

Code

ridge.cv$lambda.min

[1] 0.03770618

Generally, the purpose of regularization is to balance accuracy and simplicity. This means, a model with the smallest number of predictors that also gives a good accuracy. To this end, the function cv.glmnet() finds also the value of lambda that gives the simplest model but also lies within one standard error of the optimal value of lambda. This value is called lambda.1se.

$A

6 x 1 sparse Matrix of class "dgCMatrix"

s0

2.648144980

age -0.087712433

household 0.118887896

position_level 0.125788485

genderMale 0.441857800

absent -0.002939366

$B

6 x 1 sparse Matrix of class "dgCMatrix"

s0

0.596075835

age 0.032590386

household -0.410129801

position_level -0.106127988

genderMale -1.027268491

absent -0.001981378

$C

6 x 1 sparse Matrix of class "dgCMatrix"

s0

-3.244220816

age 0.055122047

household 0.291241905

position_level -0.019660497

genderMale 0.585410691

absent 0.004920744

Prediction test data

Code

# Make predictions on the test datax.test <-model.matrix(product~., test)[,-1]# Outcome variabley.test <-train$product# Predictionridge.pred<-as.data.frame(test$product)ridge.pred$Class_Pred<-ridge.fit |>predict(newx = x.test, type="class") ridge.pred <- ridge.pred |> dplyr::select("test$product", "Class_Pred") |> dplyr::rename(Obs_Class ="test$product") |> dplyr::rename(Pred_Class ="Class_Pred") glimpse(ridge.pred)

Rows: 438

Columns: 2

$ Obs_Class <fct> A, A, A, A, A, A, A, A, A, A, A, A, A, A, A, A, A, A, A, A,…

$ Pred_Class <chr[,1]> "A", "B", "A", "B", "B", "A", "C", "A", "A", "A", "A", …

Finally we will extract the coefficients for the selected \(λ\) using coef() function:

Code

coef(lasso.fit)

$A

6 x 1 sparse Matrix of class "dgCMatrix"

s0

3.65183352

age -0.11527181

household 0.15408964

position_level 0.06947353

genderMale 0.42949078

absent .

$B

6 x 1 sparse Matrix of class "dgCMatrix"

s0

0.21983614

age 0.04498977

household -0.49079558

position_level -0.05717795

genderMale -1.00574848

absent .

$C

6 x 1 sparse Matrix of class "dgCMatrix"

s0

-3.87166967

age 0.07028204

household 0.33670594

position_level -0.01229558

genderMale 0.57625770

absent .

Prediction test data

Code

# Make predictions on the test datax.test <-model.matrix(product~., test)[,-1]# Outcome variabley.test <-train$product# Prediction# Predictionlasso.pred<-as.data.frame(test$product)lasso.pred$Class_Pred<-lasso.fit |>predict(newx = x.test, type="class") lasso.pred <- lasso.pred |> dplyr::select("test$product", "Class_Pred") |> dplyr::rename(Obs_Class ="test$product") |> dplyr::rename(Pred_Class ="Class_Pred") glimpse(lasso.pred)

Rows: 438

Columns: 2

$ Obs_Class <fct> A, A, A, A, A, A, A, A, A, A, A, A, A, A, A, A, A, A, A, A,…

$ Pred_Class <chr[,1]> "A", "B", "A", "A", "B", "A", "A", "A", "A", "A", "A", …

Predicted

Actual A B C

A 125 18 6

B 26 101 11

C 20 18 113

Elastic Net Regression

Cross Validation of the best Elastic Net regression

Code

#|message: false# Define hyperparameter gridalphas <-seq(0, 1, by =0.1) # Grid for alphalambda_seq <-10^seq(3, -3, length =100) # Grid for lambda# To store resultsresults <-data.frame(alpha =numeric(), lambda =numeric(), error =numeric())# Perform grid searchfor (a in alphas) {# Fit glmnet model for each alpha cv_fit <-cv.glmnet(x.train, y.train, family ="multinomial", alpha = a, lambda = lambda_seq, type.measure ="class")# Extract best lambda and error for the current alpha best_lambda <- cv_fit$lambda.min best_error <-min(cv_fit$cvm) # Minimum cross-validation error# Store results results <-rbind(results, data.frame(alpha = a, lambda = best_lambda, error = best_error))}# Find the best parametersbest_params <- results[which.min(results$error), ]print(best_params)

alpha lambda error

2 0.1 0.00231013 0.2247525

Fit the final model with optimal parameters

Code

# Refit the final model with optimal parametersenet.fit <-glmnet(x.train, y.train, family ="multinomial", alpha = best_params$alpha, lambda = best_params$lambda)# View coefficientsprint(coef(enet.fit))

$A

6 x 1 sparse Matrix of class "dgCMatrix"

s0

4.699700666

age -0.166665301

household 0.228786494

position_level 0.261680332

genderMale 0.614902899

absent -0.007895397

$B

6 x 1 sparse Matrix of class "dgCMatrix"

s0

0.28951435

age 0.06737238

household -0.69844870

position_level -0.15111152

genderMale -1.58434184

absent .

$C

6 x 1 sparse Matrix of class "dgCMatrix"

s0

-4.989215017

age 0.091022644

household 0.419403184

position_level -0.019721577

genderMale 0.741220510

absent 0.005142852

Prediction test data

Code

# Make predictions on the test datax.test <-model.matrix(product~., test)[,-1]# Outcome variabley.test <-train$product# Predictionenet.pred<-as.data.frame(test$product)enet.pred$Class_Pred<-enet.fit |>predict(newx = x.test, type="class") enet.pred <- enet.pred |> dplyr::select("test$product", "Class_Pred") |> dplyr::rename(Obs_Class ="test$product") |> dplyr::rename(Pred_Class ="Class_Pred") glimpse(enet.pred)

Rows: 438

Columns: 2

$ Obs_Class <fct> A, A, A, A, A, A, A, A, A, A, A, A, A, A, A, A, A, A, A, A,…

$ Pred_Class <chr[,1]> "A", "B", "A", "B", "B", "A", "C", "A", "A", "A", "A", …

Predicted

Actual A B C

A 119 20 10

B 25 102 11

C 19 20 112

Summary and Conclusion

In this tutorial, we explored regularized multinomial logistic regression in R, focusing on both the manual implementation and using the efficient {glmnet} package. We began by understanding the fundamentals of multinomial logistic regression, a model used for predicting categorical outcomes with more than two classes. Recognizing that overfitting can be a significant issue in high-dimensional or small datasets, we introduced regularization techniques, specifically Ridge (L2) and Lasso (L1) regression, which add penalty terms to the model to prevent overfitting and improve generalization. This process may entail parameter tuning through grid search, facilitated by the {caret} or {h2o} packages (please refer to the Machine Learning chapter).